FinTech Ecosystems: A Detailed Guide to Transform Finance

Forget dusty bank vaults and endless paperwork – finance is having a revolution, propelled by a rocket named “FinTech.”

FinTech, or financial technology, is transforming the way you handle money, making financial services faster, easier, and more accessible.

But FinTech isn’t just a solo act. It thrives in vibrant hubs called FinTech ecosystems.

In this guide from Designveloper, you’ll explore the world of FinTech and FinTech ecosystems by looking at its current growth and emerging trends. Also, the article will discuss the top technologies being applied and the challenges these ecosystems face.

So, if you’re aiming to carve out your niche in FinTech or just curious about how technology is reshaping finance, this guide is for you. Let’s read on!

What is FinTech?

FinTech, short for Financial Technology, is the integration of modern technology into financial services to improve their use and delivery.

The core goals of FinTech are to simplify, automate, and improve financial tasks that were traditionally complex and time-consuming. This includes everything from transferring money to friends to managing investments or applying for a loan.

One standout example of FinTech is mobile banking. With just a few taps on a smartphone, users can check their balance, pay bills, transfer money, and even deposit checks. Thanks to technology, your financial life becomes easier, more efficient, and more convenient. So, when using your banking app, you’re experiencing FinTech in action!

What are FinTech Ecosystems?

FinTech ecosystems are collaborative environments where startups, tech companies, and financial institutions work together to drive innovation.

Types of FinTech Ecosystems

FinTech ecosystems can be generally categorized into four key types:

International Financial Hubs: Centres like New York, London, Paris, or Singapore are international financial hubs where FinTech ecosystems thrive due to the large scale of these centers and easy access to talent and capital. Consumer protection regulation is often a top priority for policymakers in these centers.

Regional Financial Hubs: In such centers as Amsterdam or Stockholm, FinTech ecosystems often receive substantial government support. However, they may face a shortage of talent and rely heavily on international connections for expansion.

Emerging Financial Hubs: These centers, typically Abu Dhabi, are characterized by a severe lack of talent and internal connections. Despite these challenges, they often receive strong government support, with a regulatory focus from policymakers.

Non-Financial Tech Hubs: FinTech ecosystems have also emerged in cities that are major tech hubs, such as Silicon Valley, Berlin, and Hangzhou. These hubs have significant access to technical talent and capital but may lack a comprehensive understanding of financial institutions.

FURTHER READING: |

1. Fintech AI Risks: 8 AI Challenges Fintechs Still Struggle With |

2. What is a SaaS Product: Features, Trends & Examples |

3. SaaS Application Development: A 6-Step Guide |

How FinTech Ecosystems Work

To understand the way FinTech ecosystems operate, let’s take a look at Singapore.

In particular, Singapore offers a dynamic playground for various stakeholders to conduct financial services digitally. These stakeholders include:

- Startups (like StashAway and SingXpress)

- Established players (like DBS Bank and Temasek)

- Tech innovators (like Fave and Zilliqa)

All these entities collaborate under the supportive regulatory environment fostered by the Monetary Authority of Singapore (MAS) to ensure financial stability and security.

For instance, DBS partners with StashAway for robo-advisory services while Fave integrates with Zilliqa for secure micro-payments.

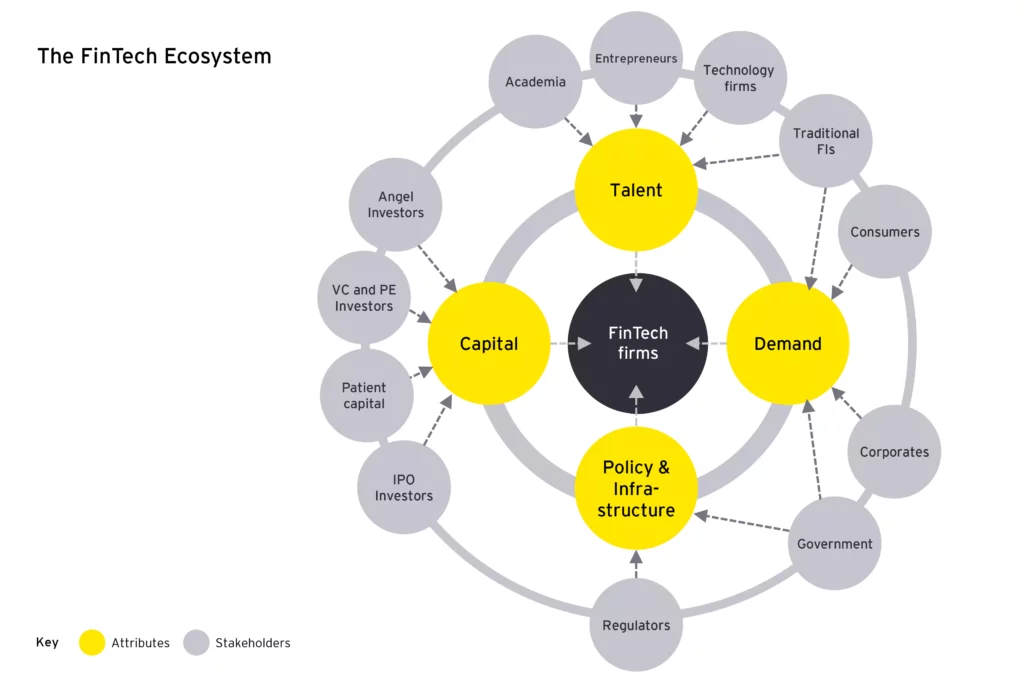

Common Attributes Influencing the Development of FinTech Ecosystems

From the EY team’s perspective, a successful FinTech ecosystem is underpinned by four key attributes: Talent, Demand, Capital, and Policy & Infrastructure.

Now, let’s delve into each of these elements:

Demand

The Internet and mobile devices are booming. This leads to a stronger demand for new financial products and services offered digitally over traditional ones.

This demand has promoted online financial transactions (e.g., loans or investments), hence requiring a creditable FinTech ecosystem to facilitate these activities.

Apart from individual and organizational customers, demand for FinTech services also involves other stakeholders:

- Traditional Financial Institutions (FIs): Banks and other established players, spurred by the buzz of demand, adapt and innovate. They launch digital offerings, partner with FinTech startups, and strive to offer the services that keep their customers happy.

- FinTech Startups: Nimble and agile, they see the demand as an open door, launching innovative products and services that cater to specific needs, from micro-investments to robo-advisors and on-demand insurance.

- Governments: By fostering FinTech innovation, they can create accessible financial services for everyone, driving economic growth and stability.

Talent

The presence of strong founding teams and talent is a direct contributor to the success of FinTech ecosystems.

Such talents can be skilled developers, investors, and entrepreneurs who come from the following sources:

- Academia: Universities and colleges produce skilled developers through rigorous training programs and research initiatives. They also foster innovation through incubators and startup accelerators.

- Technology Firms: These companies provide the necessary tools and platforms for developers to build FinTech solutions. They also offer collaboration opportunities, allowing FinTech startups to leverage their technological expertise and resources.

- Traditional Financial Institutions (FIs): These FIs can bridge the gap between the old and the new by attracting experienced financial professionals into the FinTech world. They also partner with startups, invest in FinTech ventures, and implement FinTech solutions within their operations.

Capital

The availability of various forms of capital is also crucial for the vibrancy of FinTech ecosystems. This includes a financing chain that supports ventures from the early seed stages to the later growth stages and finally to exit.

Such financial support comes from different sources, including angel investors, Venture Capital (VC) & Private Equity (PE) investors, IPO investors, and even crowdfunding platforms.

Policy and Infrastructure

Financial services are subject to significant regulatory oversight. Laws, the regulatory environment, competition policies, and access to the regulator significantly influence the success of FinTech ecosystems. Through these policies, regulators create a supportive regulatory environment for FinTech innovation while ensuring consumer protection and financial stability.

Besides, technical infrastructure and other operational resources are also essential to fostering FinTech innovation. Organizations, including incumbents and tech companies, provide the necessary resources and robust techs (like Cloud computing and APIs) to enable the development and deployment of FinTech solutions.

FinTech Landscape: Current State & Emerging Trends

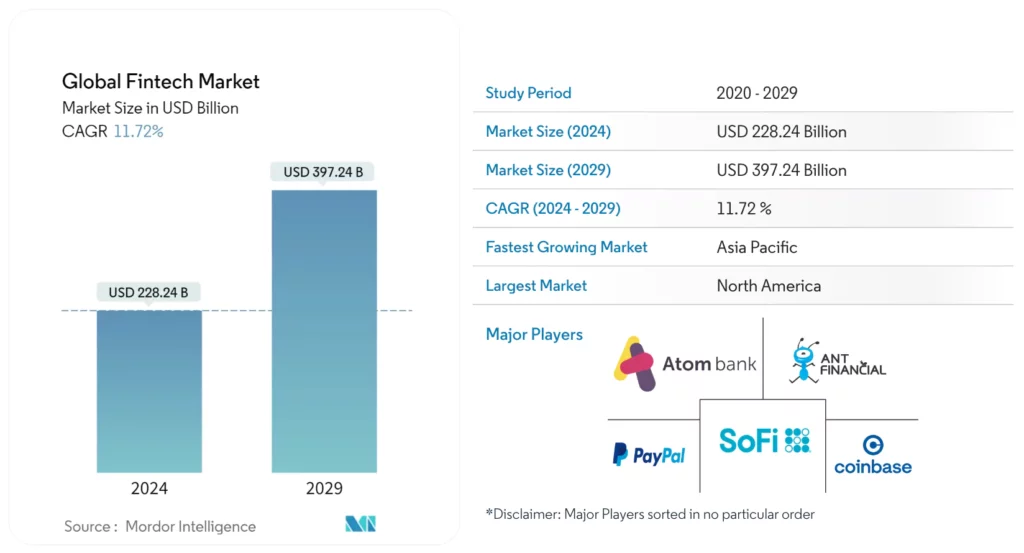

The global FinTech market, valued at USD 228.24 billion in 2024, is projected to reach USD 397.24 billion by 2029. This industry is a customer-centric powerhouse of companies ranging from startups to tech giants (like Ant Financial, Adeyn, or Paytm) vying for a place in the market.

Crises, including the global financial crisis and COVID-19, have spurred the growth of FinTech. The industry’s expansion was a response to the shortcomings of traditional financial services, which were under pressure during these crises. In the wake of COVID-19, collaborations between large financial institutions and emerging tech companies accelerated the industry’s development.

Despite facing a challenging future, the FinTech industry is poised for growth. McKinsey’s research indicates that FinTech revenues are expected to grow nearly three times faster than those in the traditional banking sector between 2022 and 2028. The industry is entering a new era of value creation, focusing on sustainable, profitable growth.

As you look ahead, the FinTech landscape continues to evolve, with emerging trends set to further transform the industry. Stay tuned as we delve into these trends in our upcoming discussion.

Neobanks

Neobanks, also known as digital-only banks, are a new breed of financial technology firms. They offer banking services primarily through digital platforms such as mobile apps or websites. These institutions, often startups, operate without physical branches, aiming to streamline banking services by offering a seamless online experience, lower fees, and more competitive rates than traditional banks.

The rise of neobanks has significantly impacted traditional banking models. They have introduced a customer-centric approach that has led to the transformation of companies into more agile and responsive entities.

The advent of neobanks represents a paradigm shift in the financial services industry, challenging the status quo and pushing the boundaries of what is possible in the banking sector.

Decentralized Finance (DeFi)

DeFi uses blockchain technology and cryptocurrencies to recreate and improve upon traditional financial systems.

Accordingly, DeFi platforms leverage smart contracts on blockchain networks, allowing users to lend, borrow, trade, earn interest, and even take out insurance directly from each other. This direct interaction can lead to more efficient markets, lower costs, and greater access to financial services.

The potential of DeFi to disrupt financial services is immense. By eliminating intermediaries (like banks or brokerages), DeFi democratizes access to financial services, making them available to anyone with an internet connection. It also introduces unprecedented transparency and resistance to censorship in financial transactions.

However, DeFi comes with its own set of challenges and risks, including regulatory uncertainty and the technical complexities of blockchain technology. Despite these challenges, the potential benefits of DeFi make it a trend worth watching in FinTech ecosystems.

Embedded Finance

This trend involves the seamless integration of financial services into non-financial platforms, such as e-commerce sites. One popular example of this trend is Uber, a ride-hailing app that enables embedded payments.

The growth of embedded finance is driven by customer-facing businesses that aim to control the end-to-end user experience. By embedding financial services directly into their platforms, these businesses can offer a more streamlined and convenient service to their customers.

From 2022 to 2028, global funding for BaaS and embedded finance saw a robust growth of 36%, indicating the increasing demand and potential of these services. As more businesses adopt this model, we can expect to see a continued expansion of financial services.

InsurTech

As the name states, InsurTech exploits the power of advanced technologies such as IoT, big data, or AI to redefine traditional insurance operations.

Valued at a substantial USD 3.1 billion in 2023, the InsurTech sector is projected to grow at a CAGR of 16.53% from 2024 to 2032. This rapid expansion marks a significant paradigm shift in the FinTech landscape.

By leveraging real-time data analysis, InsurTech can provide more precise pricing and risk assessment, hence minimizing potential fraud and losses for insurance companies.

Longevity-focused finance is also gaining traction within InsurTech and wealthtech. Companies like Abacus pair alternative asset management with advanced underwriting analytics to transform life insurance and longevity data into investable, transparency-first products. By connecting technology, advisory services, and capital providers, they enable lifespan-based planning—policy valuations, portfolio construction, and ongoing servicing—grounded in regulated workflows. This approach illustrates how FinTech ecosystems help niche players scale longevity-based investments while delivering AI-powered personalization and clearer reporting for both investors and policyholders.

Top 5 Technologies Applied in FinTech Ecosystems

In the rapidly evolving world of financial technology, certain key technologies have emerged as game-changers. These techs are not only transforming traditional financial services but are also at the heart of innovative FinTech ecosystems.

This section will delve into the top five technologies that are making significant impacts in FinTech ecosystems.

Artificial Intelligence (AI)

In 2022, artificial intelligence (AI) was the most widely used tech in FinTech, accounting for about 42.82% of the market share.

AI’s role in the FinTech sector is multifaceted and transformative. Here are some key applications:

Fraud Detection: AI algorithms can analyze patterns and detect anomalies in transaction data, thereby identifying potential fraudulent activities. This proactive approach enhances security and builds customer trust.

Personalized Finance: AI can deliver personalized financial advice and product recommendations based on individual customer profiles and behavior patterns. This level of personalization improves customer experience and fosters loyalty.

Robo-advisors: AI-powered robo-advisors provide automated, algorithm-driven financial planning services with little to no human supervision. They offer a cost-effective alternative for customers seeking investment advice, portfolio management, and other financial planning services.

Blockchain

Blockchain technology is redefining the FinTech landscape by offering solutions that are secure, transparent, and efficient. Here’s how it works and its transformative potential in various areas:

Payments: Blockchain provides a decentralized ledger for recording transactions, eliminating the need for intermediaries in payment processing. This leads to faster, cheaper, and more secure transactions, especially for cross-border payments.

Identity Management: Blockchain can create immutable and verifiable digital identities, reducing fraud and enhancing KYC (Know Your Customer) processes. Customers can control their personal data and choose who to share it with.

Data Security: The decentralized and encrypted nature of blockchain makes it highly resistant to hacking. Each block contains a cryptographic hash of the previous block, making the blockchain tamper-evident. This ensures the integrity and security of financial data.

Cloud Computing

In 2022, cloud computing held a share of approximately 26.82% in the FinTech market. This indicated that a significant portion of resources were still deployed within an organization’s on-premises infrastructure.

However, the application of cloud computing in FinTech ecosystems is projected to skyrocket, reaching an estimated value of $196.2 billion by 2031. This growth can be attributed to the numerous benefits that cloud computing brings to the financial sector:

Scalability: Cloud computing enables financial companies to scale quickly and effortlessly.

Enhanced System Capabilities: Cloud computing enhances the capabilities of existing systems, speeding up data processing. This results in improved operational efficiency and better service delivery.

Cost and Configuration Efficiency: The implementation of cloud computing reduces infrastructure expenses and streamlines configuration processes. It also addresses security and compliance issues, making it a cost-effective strategy for FinTech firms.

Flexibility and Agility: Cloud computing allows FinTech firms to utilize virtual resources and services available online, negating the need for physical infrastructure. This provides flexibility in resource distribution, enabling FinTech companies to adjust their operations based on demand. Additionally, this tech boosts speed in rolling out new services and applications. It then empowers FinTech firms to quickly design and introduce innovative solutions, test new products, and adapt promptly to market shifts.

Big Data & Analytics

In a bustling FinTech world full of unorganized information, data analytics is a powerful tool to transform vast datasets into actionable insights. This, accordingly, changes the way financial services operate and deliver value to customers. Here’s how:

Driving Insights: Big Data refers to the vast volumes of structured and unstructured data generated every second. Analytics tools can process this data to uncover patterns, correlations, and trends. These insights can inform decision-making, optimize operations, and identify new opportunities in the FinTech sector.

Personalized Financial Experiences: By analyzing customer behavior, preferences, and financial history, FinTech companies can offer personalized services. This could range from tailored financial advice to customized product recommendations, enhancing customer satisfaction and loyalty.

Risk Management: Big Data and Analytics can also aid in risk assessment and management. By analyzing historical data and market trends, FinTech companies can predict potential risks and take proactive measures to mitigate them. This is particularly useful in areas like credit scoring, loan underwriting, and investment risk assessment.

CyberSecurity Solutions

In FinTech ecosystems, data security and privacy have emerged as paramount concerns. With the increasing digitization of financial services, the need for robust cybersecurity solutions has never been more critical.

Cybersecurity technology plays a pivotal role in safeguarding sensitive customer data and ensuring the integrity of financial transactions. It employs a range of security technologies, including biometrics and identity management systems, to fortify the defenses of FinTech companies against cyber threats.

Biometrics: Biometric technology includes fingerprint scanning, facial recognition, and voice recognition. This tech provides an additional layer of security by verifying the identity of users based on their unique physical or behavioral characteristics. It then significantly reduces the risk of unauthorized access and identity theft, thereby enhancing the security of customer data.

Identity Management: Identity management systems are crucial in controlling user access to critical information. These systems verify the identity of users, manage user credentials, and ensure that users only have access to the data and services they are authorized to use. By effectively managing user identities, these systems play a vital role in preventing data breaches and maintaining the confidentiality of customer information.

3 Challenges for FinTech Ecosystems

Given the nature of sensitive data, FinTech ecosystems inevitably face a myriad of challenges. As you delve into this complex landscape, you must acknowledge and embrace these challenges as opportunities for growth and innovation.

In the following sections, let’s explore significant challenges for these ecosystems.

Regulatory Hurdles

In FinTech, one of the most significant challenges lies in navigating the complex and ever-changing regulatory environment.

With the increasing prevalence of data breaches, regulations around data privacy and security have tightened. As such, FinTech companies are required to strictly abide by such regulations as Anti-Money Laundering (AML) and Know Your Customer (KYC) to prevent fraudulent activities and avoid hefty penalties.

Besides, the regulatory landscape for FinTech is rapidly evolving, with new rules and guidelines being introduced frequently. Keeping up with these changes and ensuring compliance can be a daunting task for FinTech companies.

Turn Regulations Into Opportunities

While entrepreneurs often view regulation as a barrier to innovation, those in the FinTech sector have a more nuanced perspective.

They understand that regulatory clarity can reduce uncertainty for FinTech ventures, and that regulatory approval can serve as a signal of legitimacy for startups. Furthermore, the stability of the financial system, which regulations help ensure, benefits all market participants, especially ventures with limited resources.

Policymakers can support the entry and growth of new ventures, foster collaboration among ecosystem participants, pilot new solutions, and educate consumers through various facilitation, collaboration, communication, and education activities.

The influence of financial innovations is profound, affecting not just economic structures, but also societal infrastructures at their core. This gives policymakers in FinTech ecosystems a more complex role compared to other tech ecosystems.

Besides their traditional roles as regulators and promoters of FinTech innovations, policymakers also find themselves as market participants or consumers in certain FinTech segments, such as “RegTech” and “GovTech”. This turns policymakers from mere issuers of laws into trusted partners of FinTech companies.

For this reason, regulatory hurdles, while posing significant challenges in the FinTech ecosystem, also present unique opportunities. By fostering a collaborative environment between regulators and industry players, we can turn these challenges into catalysts for innovation and growth, ultimately creating a supportive and thriving FinTech ecosystem.

Disruptive Forces

Another challenge for FinTech ecosystems is disruption. The following forces, often unpredictable and potent, can impact the FinTech landscape in profound ways:

Cybersecurity Threats: As FinTech companies increasingly rely on digital platforms and technologies, they become attractive targets for cybercriminals. Cybersecurity threats, such as data breaches and hacking, can undermine trust and cause significant financial and reputational damage.

Privacy Concerns: With the proliferation of data-driven services, privacy concerns have come to the forefront. FinTech companies must ensure they are not only compliant with data protection regulations but also able to earn the trust of their users by demonstrating a commitment to privacy.

Emergence of New Technologies: The rapid pace of technological innovation can be both an opportunity and a challenge for FinTech companies. While new technologies can open up new avenues for growth, they can also disrupt existing business models and create uncertainty.

Collaboration Between FinTech Start-ups and Incumbents

The success of FinTech ecosystems is largely dependent on how incumbent financial institutions assist start-ups by granting access to essential resources. These resources can include customer relationships, financial data, and technical infrastructure.

Start-ups face the challenge of collaborating with incumbents to gain access to these resources. Conversely, incumbents are faced with a series of strategic trade-offs. The advantages of partnering with start-ups can be significant, but not immediately evident.

Further, this partnership confronts several obstacles as follows:

Operational Issues: FinTech start-ups and incumbents often report several operational problems related to their collaboration. These can range from a lack of standards for due diligence and onboarding practices to difficulties with technical interfaces and outdated IT systems.

Limitations of Partnership Agreements: The benefits of collaboration are usually confined within narrowly defined partnership agreements. These agreements explicitly restrict the information and learning, thereby limiting the potential for these benefits to spill over into the wider ecosystem.

Diverging Objectives: Lastly, collaborations often falter due to a misalignment in the goals of incumbents and FinTech start-ups. This divergence in objectives can pose a significant challenge to successful collaboration.

Conclusion: Is There Any Space for FinTech Startups?

FinTech ecosystems are undeniably a catalyst for innovation and transformation in the financial services industry. It is not just reshaping the way you conduct financial transactions, but also redefining the very structure of the financial market.

In the current landscape, incumbents with a long history in the market are embracing emerging technologies to broaden their horizons. On the flip side, FinTech startups are leveraging partnerships with these traditional players to accelerate their growth and expand their market presence. This symbiotic relationship is not only beneficial for the parties involved but also instrumental in driving the industry forward.

Therefore, despite the possible challenges, the future for FinTech startups in this industry is still promising. The continuous evolution of technology and the increasing demand for more efficient and customer-centric financial solutions provide a fertile ground for startups to thrive. The question is not whether there is space for your FinTech startup, but rather how you can best position yourself to seize the opportunities that lie ahead.

Your involvement, whether as an entrepreneur, investor, or consumer, can contribute significantly to the success and advancement of the FinTech industry. So, let’s embrace the change, contribute to the growth, and be a part of the exciting journey that lies ahead in the world of FinTech.

Also published on

Share post on

Related Articles

25 Fintech App Ideas for New Business to Consider in 2026

25 Fintech App Ideas for New Business to Consider in 2026 Published November 24, 2025

How to Build a Debt Management Software

How to Build a Debt Management Software Published April 16, 2025

Fintech Cybersecurity: Security Measures for Robust Fintech App Development

Fintech Cybersecurity: Security Measures for Robust Fintech App Development Published May 28, 2024